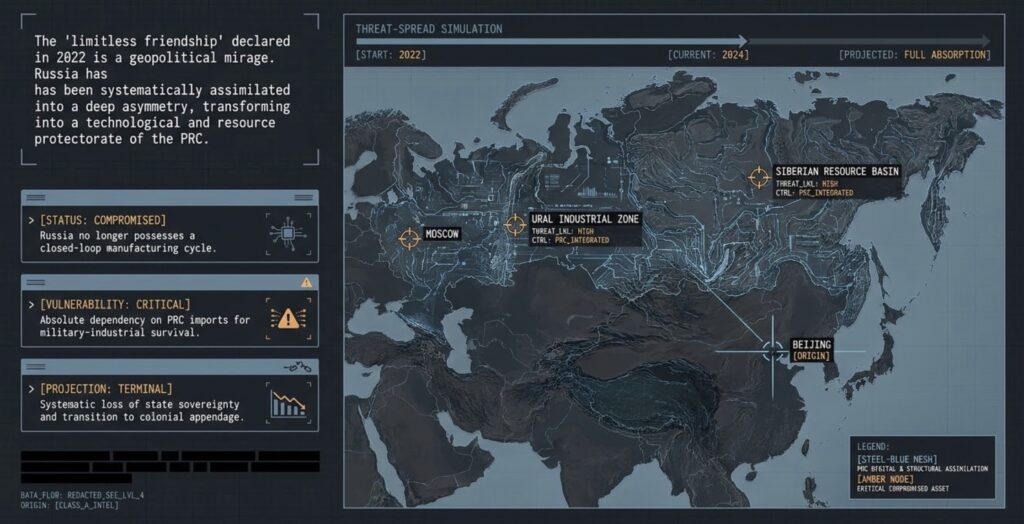

1. Introduction: The Geopolitical Trap of “Limitless Friendship”

In the contemporary geopolitical landscape of the 21st century, relations between the Russian Federation and the People’s Republic of China (PRC) have undergone a swift evolution, transforming from a declared strategic partnership into a deeply asymmetric technological and resource protectorate. The launch of the full-scale invasion of Ukraine in February 2022 and the subsequent wave of unprecedented international sanctions have permanently dismantled Moscow’s economic multi-vector foreign policy, locking it into the infrastructural and financial trap of Beijing. Today, we are witnessing not merely the replacement of Western brands with Chinese equivalents, but a sequential, systemic absorption of the Russian economy, where the PRC controls basic means of production, financial infrastructure, telecommunications, and strategic resources. This creates a threat of the complete loss of Russian state sovereignty and its gradual transformation into a colonial appendage of China.

Analysis of the dynamics of this expansion indicates that Beijing acts pragmatically and deliberately, avoiding direct clashes with Western sanction coalitions while systematically converting the geopolitical weakness of the Kremlin into long-term economic preferences. Russia’s strategic sectors, including the defense-industrial complex (DIC), the high-tech sphere, artificial intelligence (AI), and rare earth elements (REE) extraction, have de facto lost their technological sovereignty. The Russian state can only maintain its current vital functions through Chinese imports, leaving it entirely unable to establish competitive closed production cycles. This report provides a detailed retrospective analysis of this process starting from 2010, details the current state of dependency, and formulates a strategic forecast for the next five years (2026–2031), taking into account the ongoing strikes of the Armed Forces of Ukraine on Russian critical infrastructure, the weakening of central power in the RF, and the inevitability of the future transition of power in Moscow. We conclude that under the conditions of the complete fiasco of the Putin regime, Ukraine can become the sole locomotive for preserving the authenticity of the peoples of Russia.

2. Historical Retrospective of Absorption (2010–2022)

2.1. Phase of Soft Infiltration and Resource Integration (2010–2014)

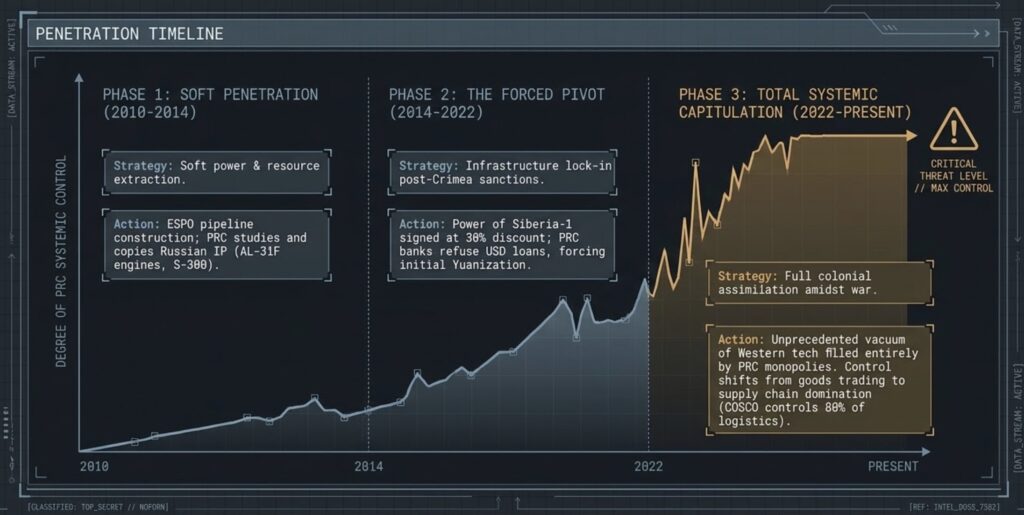

At the beginning of the second decade of the 21st century (2010–2014), the Chinese strategy toward Russia was based on the principles of soft power and the gradual expansion of its presence in the energy market. At this stage, the Russian political elite still harbored illusions of their equal standing in bilateral relations, relying on high global oil and gas prices and maintaining stable access to European export markets and European technologies. Chinese investments were directed primarily into the extraction sector of the Far East and Siberia. The construction of the Eastern Siberia – Pacific Ocean (ESPO) oil pipeline opened up the possibility of partial export diversification for the RF, but simultaneously laid the first bricks of infrastructural linkage to a single large Asian buyer. The PRC’s share in the foreign trade turnover of the RF in 2010 was about 10%, which, although making China an important partner, did not allow it to dictate its own terms of the game. During this period, China actively studied the Russian market and established bridgeheads for future technological and infrastructural dominance.

During this phase, Chinese companies actively acquired logging licenses in Siberia and established joint ventures in the agricultural sector of the Primorsky Krai. The Russian side viewed these steps as attracting foreign investment, but Beijing was creating closed economic zones using Chinese labor, Chinese equipment, and exporting all raw materials directly to the PRC without establishing processing capacities in Russia. In the technology sphere, Russia still held an advantage, selling aircraft engines (AL-31F and D-30KP series) and air defense system elements (S-300) to China, but China systematically reverse-engineered these developments, preparing for complete technological autonomy from the RF. Chinese engineers meticulously analyzed the design of Russian turbines and radars to replace them with domestic developments under the modernization program of the People’s Liberation Army (PLA).

An important aspect of this period was the agreement on the joint development of transboundary oil and coal deposits, signed during Hu Jintao’s visit to Moscow in 2011. The Chinese state corporation CNPC gained exclusive access to Russian mineral resources in exchange for a promise to finance infrastructure. However, as it turned out later, the credit lines were issued against the collateral of future oil deliveries under a formula that excluded Russia from receiving windfall profits in the event of rising global prices. The Russian side effectively agreed to the role of a resource donor in exchange for political declarations about the formation of a multipolar world. All major infrastructure projects on Russian territory were built by Chinese contractors using their own materials and equipment, which minimized the multiplicative effect for Russian domestic industry.

2.2. Phase of Forced “Pivot to the East” (2014–2022)

The annexation of Crimea by the Russian Federation in 2014 and the first Western sanctions became a turning point, forcing the Kremlin to declare a large-scale ‘pivot to the East‘. It was then that Beijing realized time was working in its favor and began to dictate much harsher terms of cooperation. The most striking example was the signing of a 30-year gas contract for the supply of fuel through the ‘Power of Siberia-1‘ pipeline. The negotiations, which had lasted for over ten years, were hastily concluded by Moscow in May 2014 on terms that remain classified, but, according to leading analysts, stipulate a critically low gas price with a discount of over 30% compared to European prices at the time. Throughout this phase, the Kremlin attempted to imitate an ‘import substitution’ policy, but de facto ‘China-substitution‘ was occurring: European industrial equipment and consumer goods were being massively replaced by Chinese brands. By 2021, China’s share in Russian imports had grown to 25%, and in the electronics and telecommunications equipment sector, it exceeded 50%.

Sanction pressure after 2014 forced the Russian government to seek funding from major Chinese banks. However, Russian hopes for limitless loans from the People’s Bank of China and PRC commercial banks quickly vanished. Chinese financial institutions strictly adhered to US and European sanctions, denying long-term foreign currency loans to Russian state-owned companies. Instead, China offered settlements in national currencies (yuan), which initiated the yuanization of Russian reserves. In the defense sector, China effectively halted purchases of finished Russian military hardware, shifting to copying Su-35 fighters (creating the Shenyang J-11/J-16 analogs) and S-400 air defense systems, which deprived Russia of significant export revenues in favor of China’s own domestic industry.

To demonstrate the success of the pivot to the East, Russian propaganda actively highlighted joint projects, such as the construction of the Nizhneleninskoye – Tongjiang bridge across the Amur River and the Blagoveshchensk – Heihe bridge. However, construction on the Russian side was constantly delayed due to corruption and funding deficits, while the Chinese side erected its spans in a matter of months. When the bridges finally opened, it became clear that cargo transit conditions were entirely regulated by Chinese customs, which introduced strict quotas on the import of Russian products. Russian timber and coal exporters found themselves in long queues, while Chinese consumer goods passed customs control under a simplified procedure. This clearly demonstrated that the infrastructure was created by Beijing solely for its own expansion.

3. The Turning Point: The Russian Economy Post-February 2022

The full-scale invasion of Ukraine by the RF on February 24, 2022, triggered the final dismantling of Russia’s integration into the global financial and economic system of the West. Sanctions, the freezing of the gold and foreign exchange reserves of the Central Bank of the RF, the disconnection of leading banks from the SWIFT system, and the exit of over 1,000 multinational corporations created an unprecedented supply vacuum. In this critical situation, China became Moscow’s sole window to the world, allowing Beijing to transition from a strategy of partnership to direct economic colonization. Russia’s dependence became systemic and all-encompassing. The Russian Federation transformed into a resource appendage of China, forced to sell Urals crude, coal, and liquefied natural gas at massive discounts, while buying finished high-value-added products in return.

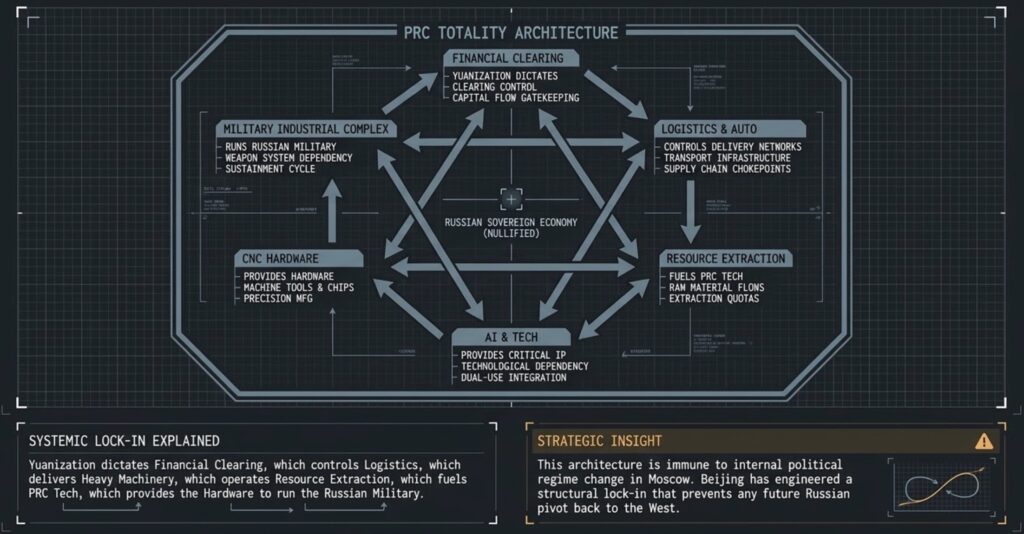

A key feature of this stage is that the level of absorption is directly dependent on the military failures of the RF. Each defeat of the Russian army on the battlefield in Ukraine, each successful operation of the AFU, and each tightening of international pressure weakens the Kremlin’s negotiating positions. The Russian leadership is willing to sacrifice the strategic interests of the state in exchange for tactical support from the PRC in the form of microchip supplies, machine tools, and financial clearing. Beijing deliberately does not rush to save the Russian economy from sanction pressure; instead, it methodically builds the infrastructure of long-term dominance, making any future pivot of Russia back toward the West impossible, even in the event of a change in the political regime. Moscow is forced to agree to unprecedented concessions, including opening its strategic markets to the expansion of Chinese state-owned enterprises.

The dynamics of absorption after 2022 are characterized by a transition from trading finished goods to establishing control over supply chains. Russian business has lost the ability to directly access global markets, as most container shipping lines (such as Maersk, MSC) terminated contracts with Russian ports. Chinese logistics companies (primarily COSCO) and small shadow carriers have seized control of over 80% of maritime and rail imports into Russia. This allowed Beijing to independently determine the priority of cargo delivery, tariffs, and supply volumes. If a Russian producer tries to compete with Chinese imports, they are simply denied rail platforms or containers on the Far East route, leading to the bankruptcy of local enterprises.

This is particularly evident in the wood processing industry of Siberia. Previously, Russian enterprises exported furniture and processed timber to Europe. After the introduction of the European embargo, the sole buyer of timber became China. Chinese buyers immediately crashed purchase prices for raw logs by 40%, while simultaneously refusing to buy processed wood. Russian wood processing plants were forced to close, and logging cooperatives fell under the direct control of Chinese firms that lease millions of hectares of taiga for symbolic sums. Russia has turned into a defenseless supplier of cheap raw materials, losing any technological added value.

4. Sectoral Analysis of Security and Infrastructure Dependency

4.1. Industrial Equipment and CNC Machine Tools

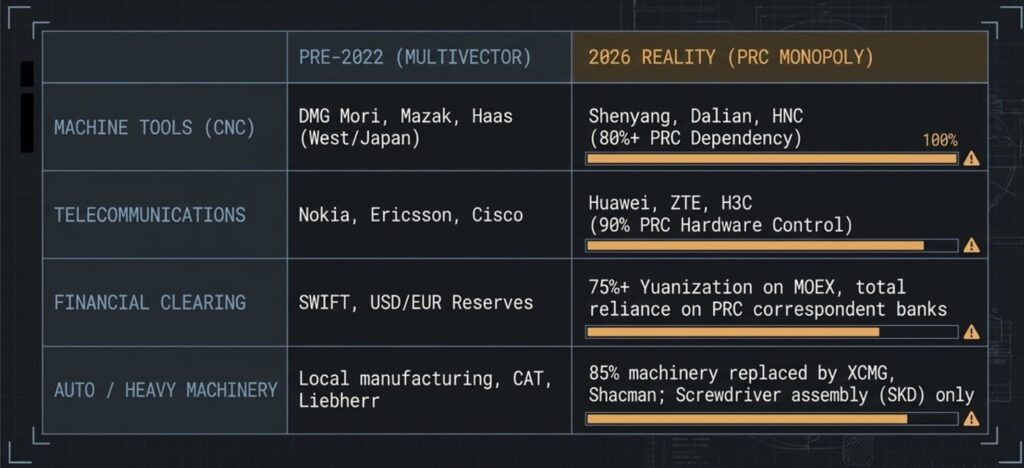

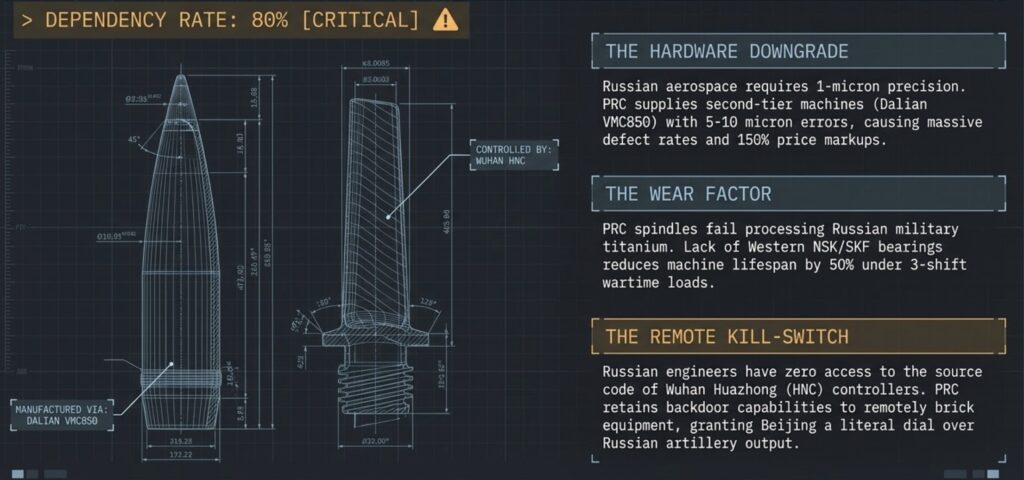

The most critical and threatening aspect for the national security of the RF is the total dependence of its defense-industrial complex on Chinese means of production. Prior to 2022, Russian military plants actively purchased advanced German, Japanese, and Italian metalworking machine tools with computer numerical control (CNC), particularly from brands like DMG Mori, Mazak, and Haas. Following the introduction of sanctions and the termination of technical maintenance for these systems, the Russian DIC faced the threat of a complete halt of production lines for artillery, armored vehicles, and aircraft engines. The only way out was an emergency reorientation toward Chinese imports. As of 2026, the share of Chinese metalworking equipment and CNC machine tools in the imports of the RF has exceeded a critical 80%.

Russian military factories now completely depend on Chinese industrial giants such as Shenyang Machine Tool and Dalian Machine Tool, as well as chip and controller systems from Wuhan Huazhong Numerical Control (HNC). Propaganda claims of machine tool production localization in the RF are a mystification: all key high-tech components (precision spindles, linear guides, servo motors, and software suites) are imported from the PRC. Furthermore, Chinese suppliers retain the capability to remotely block their equipment through embedded software backdoors, giving Beijing a direct tool of control over the production volumes and nomenclature of Russian weaponry. Russian military engineers do not have access to the source code of Chinese CNC software, leaving them hostages to Beijing’s decisions.

A critical situation has also developed in the Russian aerospace industry. The manufacture of turbine blades and fuselages for the new MS-21 and Sukhoi Superjet 100 passenger aircraft requires high-precision five-axis machine tools. China, which is itself under pressure from US and Japanese export controls, supplies second-tier machine tools to the RF. These tools have a much larger machining error (up to 5–10 microns compared to 1 micron in Japanese systems), resulting in a high percentage of defect rates at Russian defense enterprises. However, even under such conditions, Russian conglomerates Rostec and Almaz-Antey are forced to purchase equipment at prices inflated by 150%, thereby financing the technological development of the Chinese machine tool industry.

Technical specialists note that Chinese machine tools of models VMC850 and GMC2040 from Dalian Machine Tool fail en masse after just one year of operation in the three-shift mode established at Russian factories to meet front-line needs. Chinese-made spindles cannot withstand the loads when machining hard titanium alloys used in aircraft construction and armor plating. Due to sanctions, Russia cannot purchase original NSK or SKF lubricants and bearings, replacing them with cheap Chinese counterparts, which reduces the equipment’s lifespan by another 50%. As a result, the real productivity of the Russian military-industrial complex is falling, despite reports of an increase in the machine tool park. Russia pays colossal funds for low-quality imports that do not provide long-term production reliability.

4.2. Telecommunications and Technology Stack

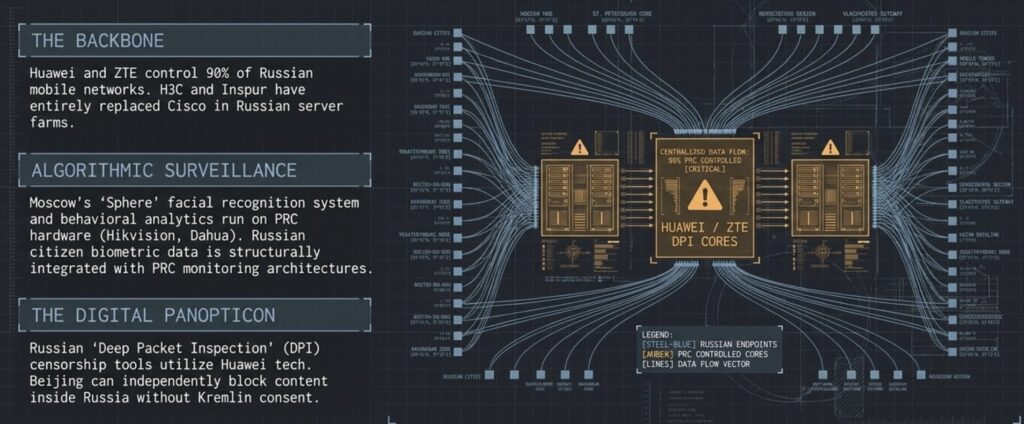

In the telecommunications sphere, Russia is experiencing a period of complete loss of infrastructural sovereignty. Following the market exit of European giants Nokia and Ericsson, which provided the construction and modernization of mobile networks, Russian telecom operators (MTS, MegaFon, Beeline, Tele2) were left without access to base stations and system software. Attempts to develop domestic 4G/5G base stations failed due to the absence of a domestic electronic component base (ECB). Consequently, Chinese corporations Huawei and ZTE became the sole suppliers of equipment for the critical telecommunications infrastructure of the RF. The share of Chinese equipment in the networks of Russian operators is approaching 90%. This means that all traffic, including state and military communications of the RF, passes through hardware systems controlled by the PRC intelligence services via official Chinese national security legislation requirements.

The replacement of network equipment affected not only mobile towers but also backbone routers and server equipment in Russian data centers. Chinese companies H3C and Inspur have completely displaced American Cisco and Juniper Networks. In 2025–2026, the entire urban video surveillance and citizen behavior analysis system in major RF cities (Moscow, St. Petersburg, Novosibirsk) transitioned to algorithms and cameras from Chinese manufacturers Hikvision and Dahua. The Russian face recognition system ‘Sfera’ de facto runs on Chinese neural network cores, integrating the Russian database into the global monitoring systems of the PRC. In the event of a conflict of interest, Beijing can paralyze the operations of the banking sector, state administration, and Russian railways in a matter of hours simply by disabling support for critical network software.

An additional threat is the transition of the Russian internet to Chinese deep packet inspection (DPI) systems. Roskomnadzor, with the help of Chinese engineers, is modernizing the TSPU (Technical Measures to Counter Threats) system, using Huawei solutions to block VPN services and independent media. This allows the Kremlin to maintain informational control inside the country, but the technological keys to this digital concentration camp are held in Beijing. If the Chinese leadership decides that certain information (for example, about the internal problems of the PRC or territorial claims against the RF) should not be distributed in the Russian segment of the internet, they can block it themselves, without the consent of Russian censors.

4.3. Automotive Sector, Commercial Transport, and Logistics

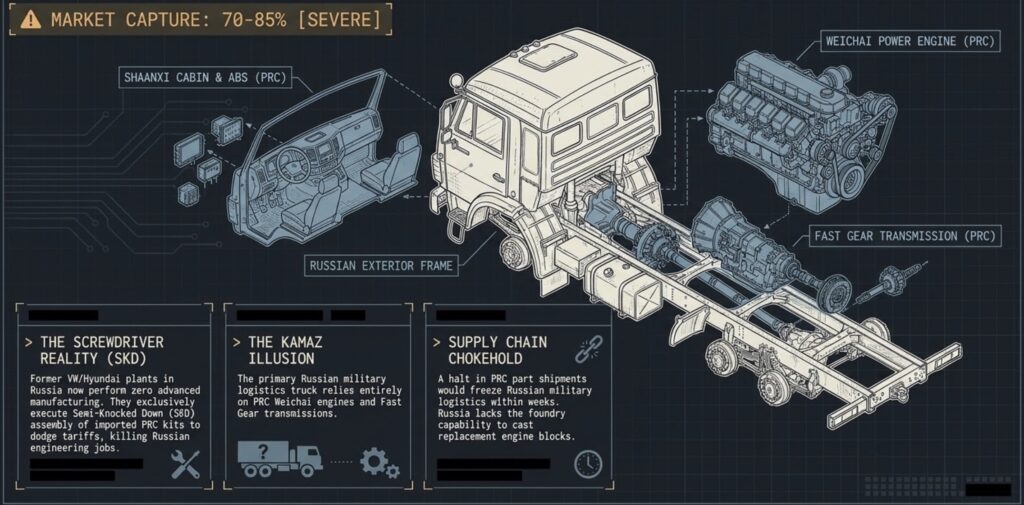

The consumer auto market in the RF underwent the fastest transformation. Instead of European, Korean, and Japanese brands, the Russian passenger car market was 70% occupied by Chinese concerns (Chery, Geely, Haval, Changan, BYD). However, much more dangerous is the expansion in the sector of heavy machinery, road construction equipment, and commercial transport. Chinese manufacturers Shacman (Shaanxi), XCMG, FAW, and Liugong displaced market leaders like Caterpillar, Liebherr, Volvo, and Komatsu from the Russian market, covering over 85% of the needs of the RF’s infrastructure projects. Even the Russian automotive giant KAMAZ and passenger car manufacturer AVTOVAZ (Lada) are unable to produce vehicles without Chinese components (braking systems, ABS, Common Rail fuel equipment, engine control units). The logistics system of the RF, including rail transportation along the BAM and Trans-Siberian railway, is oriented toward serving cargo flows to China, while the return flow is fully loaded with Chinese imports, depriving Russian local manufacturers of any chance for independent development.

Chinese automotive companies refuse to localize production in Russia, despite numerous incentives and appeals from the Ministry of Industry and Trade of the RF. At former Volkswagen, Nissan, and Hyundai plants in St. Petersburg and Kaluga, Chinese concerns have organized exclusively semi-knocked-down (SKD) assembly of cars from finished kits imported from the PRC. This allows them to avoid paying high import customs duties and recycling fees without creating any jobs for Russian engineers. All added value, welding and painting technologies, as well as the production of complex components, remain in China. Russian workers at these plants perform only primitive manual assembly operations, which locks in the technological backwardness of Russian machine building for decades to come.

In the commercial truck sector, KAMAZ was forced to abandon Daimler cabs and Cummins engines, replacing them with Chinese cabs from Shaanxi and engines from Weichai Power. The new Russian military trucks used for supplying troops on the front lines in Ukraine are de facto Chinese vehicles assembled on Russian frames. This creates enormous logistical risks for the Russian army: in the event that the supply of Weichai spare parts or Fast Gear transmission components from the PRC is cut off, Russian military logistics will grind to a halt within a few weeks, as the plants in Naberezhnye Chelny are unable to cast cylinder blocks or gears of the required quality.

4.4. Artificial Intelligence (AI), Cloud Computing, and Semiconductors

In the field of advanced technology and artificial intelligence, the RF has found itself isolated from Western computing platforms. Modern AI models require thousands of specialized graphics processors like Nvidia H100/A100 for training and inference. Due to strict US sanctions, the parallel import of these chips to the RF has become sporadic and extremely expensive (with price premiums reaching 200–300%). Russian tech giants, primarily Sberbank (with its GigaChat model) and Yandex (with its Alice AI and YandexGPT lines), are forced to migrate to Chinese hardware accelerators. The primary solution for Russian data centers is the Ascend 950PR processor from Huawei. However, access to these chips is limited: Huawei prioritizes Chinese leaders (ByteDance, Tencent, Alibaba), leaving Russian clients with only residual quotas. Moreover, the software stack of Russian AI is becoming secondary—over 85% of Russian developments are based on Chinese open-source solutions such as Qwen from Alibaba and DeepSeek, making the technological ecosystem of the RF fully dependent on the updates and architectural decisions of Chinese developers.

The complete failure of Russian projects for sovereign processors ‘Elbrus‘ and ‘Baikal‘ is illustrative. After the Taiwanese company TSMC ceased cooperation with Russian designers, Russia tried to set up chip manufacturing at its own Mikron and NIIME factories in Zelenograd. However, Russia’s technological capabilities are limited to an outdated 90–130 nanometer process, whereas modern AI processors require a topology of at least 5–7 nanometers. Attempts to purchase Chinese lithography equipment on the shadow market proved futile: the PRC is building its own plants based on SMEE lithographs and does not want to supply scarce systems to Russia in order to avoid falling under US technology sanctions. As a result, Russian developers are forced to liquidate their legal entities or relocate offices to China, transferring talent to the Chinese ecosystem.

Furthermore, Russian AI developers have encountered serious software limitations. The global standard for machine learning libraries, PyTorch and TensorFlow, is optimized for Nvidia’s CUDA architecture. Transitioning to Chinese Huawei hardware requires using their proprietary closed software environment CANN (Compute Architecture for Neural Networks). Rewriting code under CANN is accompanied by numerous errors, reduced computing speed, and the need to hire Chinese specialists to configure systems. Russian IT companies are forced to hire Chinese consultants who gain full access to the structure of Russian algorithms and internal databases. This means that Russia is unable to create a single military AI system (for example, for controlling drone swarms or analyzing satellite imagery) that would be hidden from Beijing.

5. Infrastructure Trap, REE (Rare Earth Elements), and Resource Discounts

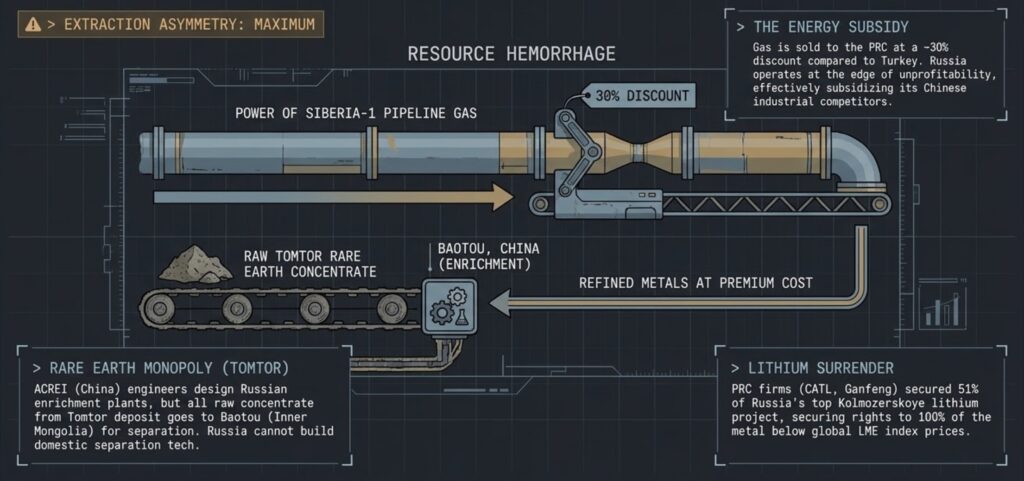

Having lost the European gas and oil market, which had formed the country’s budget for half a century, Russia found itself in absolute logistical dependence on China. This allowed Beijing to dictate unprecedentedly favorable prices for itself. The price of Russian pipeline gas for the PRC supplied through ‘Power of Siberia-1‘ is on average 28–32% lower than the price for Turkey or former European contracts. Moreover, Beijing is deliberately blocking and dragging out the construction of the new ‘Power of Siberia-2‘ pipeline, demanding the establishment of domestic Russian gas prices (which is below the cost of extraction and transportation) and shifting all capital construction costs exclusively onto Russian Gazprom, which has already recorded record losses over the past years.

China uses the geopolitical isolation of the RF to obtain exclusive rights to use the Northern Sea Route (NSR). Beijing insists on the creation of a joint consortium where Chinese shipowners will receive preferential tariffs and priority transit rights escorted by the RF’s icebreaker fleet. Furthermore, China demands the transfer of control over port infrastructure in Murmansk, Arkhangelsk, and Vladivostok, which effectively liquidates the monopoly of the Russian state concern Rosatom over Arctic transit. Russia is forced to agree to these terms, because without Chinese investments and technologies, the construction of new Arc7 ice-class Arctic tankers is impossible due to sanctions against Russian shipyards (Zvezda).

An analysis of the pricing parameters of gas supplies via ‘Power of Siberia-1’ shows that Russia receives about $210 per thousand cubic meters, while European countries in 2021–2022 purchased it at prices ranging from $400 to $1,000. Given the high capital costs of developing the Chayanda and Kovykta fields and paying VAT, Gazprom operates on the edge of profitability. Meanwhile, China uses this cheap gas to ensure the competitiveness of its own chemical and metallurgical industries, displacing Russian fertilizer and metal producers from South-East Asian markets. Russia is subsidizing its own economic competitor, which is methodically destroying Russian domestic industrial enterprises.

In parallel, China is carrying out a covert seizure of Russian strategic resources, particularly deposits of rare earth metals (REE)—neodymium, lanthanum, cerium, and lithium, which are critical for the defense industry, battery manufacturing, and electronics. Russia possesses vast REE reserves (specifically, the Tomtor deposit in Yakutia), but lacks the technology for extraction and industrial separation, since the global REE processing market is 90% controlled by the PRC. Through mechanisms of joint ventures and collateral loans, Chinese state corporations obtain monopoly rights to exploit these deposits. Russia is effectively giving away its mineral wealth without creating added value on its territory, deepening its colonial status.

In June 2025, the Russian government signed a memorandum with the Association of China Rare Earth Industry (ACREI), according to which Chinese specialists receive access to the technological maps of all Russian deposits on the Kola Peninsula and Siberia. Chinese engineers will carry out the auditing and design of enrichment plants. However, under the terms of the memorandum, the obtained REE concentrate will be exported for final separation to factories in Baotou (Inner Mongolia, PRC). Russia is deprived of the right to develop its own metal separation technologies, remaining exclusively a supplier of low-profit raw materials. This makes the Russian military-industrial complex completely dependent on supplies of separated metals from China, even for the production of its own missiles and radars.

A similar situation is observed in lithium extraction. Due to the suspension of lithium raw material imports from Chile and Argentina in 2022, Russia faced the threat of stopping battery production for military radio stations and UAVs. A joint project of Rosatom and Nornickel to develop the Kolmozerskoye deposit in the Murmansk region requires significant technology and equipment. Chinese corporations, including CATL and Ganfeng Lithium, agreed to provide technologies in exchange for a 51% stake in the future consortium and the right of first refusal for 100% of the extracted metal at prices below global exchange indices (LME). Russia has effectively lost control over its largest lithium deposit even before the start of its industrial exploitation.

6. Yuanization and Financial Dependence

The financial system of the RF has lost its sovereignty due to the forced withdrawal of so-called ‘toxic currencies’ (US dollars and euros) from circulation. The main means of settlement and accumulation of reserves has become the Chinese yuan. The share of the yuan in the trading of the currency section of the Moscow Exchange exceeded 75%, and in settlements for Russian exports to Asian countries, it is approaching 80%. The Russian Ministry of Finance and the Central Bank hold the majority of the liquid assets of the National Wealth Fund (NWF) in yuan and gold. This puts the stability of the Russian ruble and the execution of budget obligations in direct, tight dependence on the monetary policy of the People’s Bank of China and exchange rate fluctuations, which are determined in the interests of the Chinese economy, not the Russian one.

At the same time, China tightly controls Russia’s transaction flows, using US sanction pressure as a lever. During 2025–2026, large state-owned banks in China (Bank of China, ICBC, CCB, Agricultural Bank of China) catastrophically tightened compliance checks on Russian payments due to fear of falling under US secondary sanctions. They reject or block over 70% of direct transactions in yuan from the RF, even if the goods do not have a direct military purpose. This forces Russian importers to use complex shadow networks of intermediaries in third countries (Kyrgyzstan, Kazakhstan, UAE) or through small regional banks on the border with the PRC (for example, in Xinjiang province). This increases transaction costs by 8–12% and extends delivery times to several weeks, undermining the profitability of Russian business.

Since Russian banks do not have direct access to the Chinese payment system CIPS due to the threat of the latter’s disconnection from SWIFT, all settlements are carried out through Chinese correspondent banks. In 2026, the People’s Bank of China introduced restrictions on the export of cash yuan to the RF and limited the possibilities of converting yuan into dollars/euros for Russian legal entities. This led to a shortage of yuan liquidity inside the RF and a sharp increase in rates on yuan deposits (up to 12–15% per annum). Russian companies are forced to buy yuan at an inflated rate on the domestic market, which stimulates inflationary processes and depreciates the ruble. The financial system of the RF has de facto transitioned under the external management of the monetary authorities of the PRC.

A real financial disaster was the situation with opening accounts for Russian firms in branches of Russian banks in China (for example, VTB Shanghai). This branch was created to conduct direct transactions without Western correspondents. However, due to a gigantic influx of applications and the reluctance of the Chinese authorities to expand the bank’s license, the queue to open an account stretched for 3–5 months, and the fee for opening an account reached $20,000. Even after opening an account, Russian companies face the fact that Chinese counterparties refuse to accept payments from them if the sending bank is under direct US sanctions. As a result, Russian business pays huge commissions to intermediaries, which reduces the competitiveness of the Russian economy and makes it completely dependent on the compliance of Chinese regulators.

7. Five-Year Strategic Forecast (2026–2031)

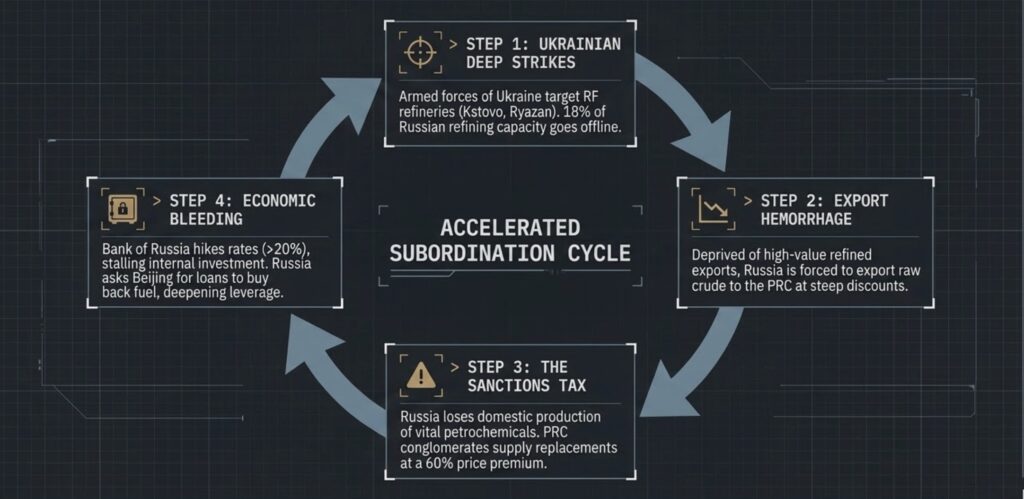

In the perspective of the next five years, the dynamics of the absorption of the Russian economy by China will be determined by the cumulative effect of the military failures of the RF in Ukraine, the destruction of its energy infrastructure, and the upcoming political transition. A key factor in the weakening of Russian export potential has been the regular and high-precision long-range strikes of the Armed Forces of Ukraine on oil refineries (refineries) and oil terminals in the European part of the RF. As of 2026, these attacks have disabled over 18% of Russian oil refining capacities. This deprives the Kremlin of the opportunity to export petroleum products with high added value (diesel, gasoline, fuel oil), forcing it to increase exports of crude oil to China and India. Since the crude oil market is limited and the PRC buys oil at a significant discount (due to the absence of alternative routes for the RF), Russian budget revenues will continue to shrink rapidly. This will accelerate the devaluation of the ruble and force the Central Bank of the RF to maintain a record-high key rate (over 20%), which will effectively halt domestic commercial lending and investment.

Due to the shutdown of refineries, Russia is forced to import high-octane motor gasoline and additives from China and Belarus, which increases fuel prices inside the country and provokes a crisis in the agricultural sector. The reduction of oil refining also leads to a shortage of aviation kerosene, which limits the capabilities of Russian civil aviation and aerospace forces. The Russian government is forced to ask China for preferential loans to purchase fuel, which gives Beijing additional leverage. During 2027–2029, the closure of over 30% of small and medium oil fields in Western Siberia is forecast due to the impossibility of exporting raw materials and the absence of hydraulic fracturing (hydraulic fracturing) technologies, which were previously supplied by US companies Halliburton and Schlumberger.

Long-range strikes by the AFU on refineries in Kirishi, Ryazan, and Kstovo resulted in Russia losing the ability to produce expensive petrochemical additives and aromatic hydrocarbons, which are raw materials for the production of explosives, plastics, and paints. Chinese chemical concerns immediately offered their supplies, but at prices that are 60% higher than global averages. This creates a ‘sanctions tax’ effect, where Russian industry pays an additional margin to China for every produced projectile or component. The Russian economy has found itself in a vicious circle: the more it fights, the weaker it becomes, and the higher the prices China sets for critical components.

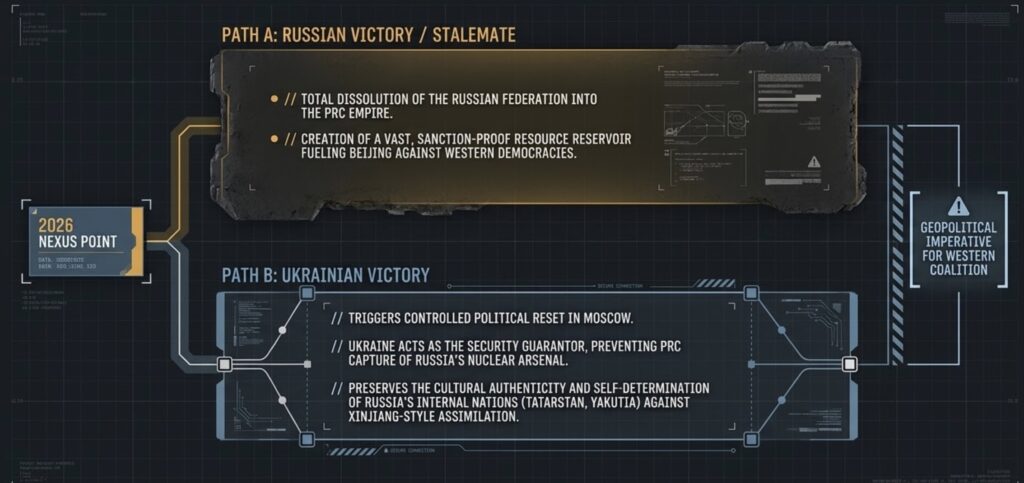

Parallel to economic exhaustion, Russia is approaching the critical phase of a socio-political transition. The aging of the governing top leadership headed by Putin, society’s fatigue from a protracted war, and the internal elite struggle for the redistribution of resources create conditions for a deep political crisis. China views this future transition not as a risk but as a strategic opportunity. Beijing’s main goal is to prevent the democratization of the RF or its exit from under Chinese influence. Beijing is preparing a scenario to establish complete political curatorship over the transitional government in Moscow. In the event of attempts at destabilization or civil conflicts in the RF, China can act as a ‘guarantor of stability’ by introducing its forces (under the guise of private military companies or peacekeeping contingents) to protect critical infrastructure—nuclear facilities, pipelines, and REE deposits in Siberia and the Far East, which will de facto mean a soft annexation of these territories.

The scenario of a ‘soft annexation’ of Siberia and the Far East relies on demographic expansion. Due to mobilization and the massive emigration of the working-age population, the border regions of the RF have suffered a demographic catastrophe. The population of Transbaikalia and the Khabarovsk Krai is declining by 1.5% annually. China, conversely, stimulates the resettlement of its citizens to the border Russian regions by providing preferential loans for the development of agriculture and business. Russian legislation on Territories of Advanced Development (TAD) allows the unhindered entry of foreign labor and the leasing of land for 49 years. By 2031, in key border cities of the RF, the share of the Chinese population may exceed 40%, creating conditions for Beijing to pursue a policy of protecting compatriots and de facto severing these regions from the federal center.

According to confidential reports of Chinese think tanks under the Ministry of State Security of the PRC, in the event of the start of a transition of power in the RF, Beijing plans to deploy the concept of ‘security corridors‘. This involves the introduction of units of the People’s Armed Police of China to guard railway mainlines (BAM and Trans-Siberian) under the pretext of protecting Chinese cargo from looting and terrorist attacks. Furthermore, China is actively working with regional elites in Yakutia, Buryatia, and the Zabaykalsky Krai, offering direct financial subsidies to local budgets in exchange for guarantees of preserving Chinese property. In the event of a collapse of central power in Moscow, Beijing will be able to carry out a de facto disintegration of the RF along the Ural ridge, subordinating the eastern part of the country to its direct administration.

8. Geopolitical Conclusion: Ukraine’s Role as the Locomotive for Preserving the Authenticity of Russia’s Peoples

The conditions of the complete internal and external collapse of the Putin regime present the Ukrainian state and the international community with a fundamental geopolitical task. The threat of complete absorption of Russia by China is a challenge not only for the Russian population itself but also for the security of all Europe, since the transformation of the RF into a gigantic vassal resource reservoir of the PRC will fundamentally change the balance of power in the global confrontation between democracies and autocracies. In this situation, Ukraine, defeating Russia on the battlefield, objectively becomes the only possible locomotive for preserving Russian statehood and the authenticity of the peoples inhabiting it. Ukraine has the potential to act not as a destroyer but as a savior of these peoples from ultimate Asian absorption.

Following Ukraine’s military victory and the beginning of the political collapse in the RF, two alternative paths of development will emerge: either the complete dissolution of Russia in the Chinese empire with the demographic absorption of Siberia and the Far East, or transition under the security umbrella of the European system, where Ukraine will act as a key guarantor of stability and revolutionary transition. The Ukrainian Armed Forces, possessing unique combat experience and geographical proximity, are capable of becoming the force that will ensure order during the chaos of power transition in Moscow, preventing Chinese structures from establishing control over the nuclear arsenal and strategic enterprises of the RF. Ukraine’s victory liberates not only its own territories; it also liberates the peoples of Russia from imperial self-destruction. The choice for the future of Russia is obvious: either the preservation of its national and cultural authenticity under the military-political guarantees of Ukraine, or ultimate death as a sovereign entity and dissolution in the Chinese neo-colonial project.

AFU guarantees will allow the peoples of the RF (both Russians and national minorities of Tatarstan, Bashkortostan, Yakutia, and the Caucasus) to preserve their own cultural codes and the right to self-determination within a new democratic confederation. Conversely, under the rule of Beijing, these peoples face harsh assimilation similar to the Uyghurs in Xinjiang—the creation of a network of re-education camps, total digital control, forced demographic mixing, and the destruction of any manifestations of national identity. Ukraine, defeating Russia, opens the doors to European civilization for it and protects it from dissolution in authoritarian China. Russian society and elites must realize: the struggle against Ukraine is a struggle for the interests of China, which leads to their own destruction, while cooperation with Ukraine is the sole chance for salvation and preserving their own future.

The establishment of transitional Ukrainian military administrations in the border regions of the RF and the provision of logistical support to new democratic governments in the regions will allow stabilizing the situation and preventing a humanitarian catastrophe. Ukraine will be able to act as a mediator between the new entities of the former RF and the world community, ensuring the lifting of sanctions in exchange for complete denuclearization and abandonment of aggressive imperial policies. Only under the security umbrella of the European coalition led by Ukraine will the peoples of the former empire be able to preserve their language, culture, and identity. Continuing the war against Ukraine only accelerates their transformation into defenseless serfs of Beijing, who will be dissolved in the billion-strong demographic sea of China without any chance of historical revival.

KRONOS Institute for Social Dynamics and Security

The investigation actively utilized OSINT tools and artificial intelligence, specifically the Gemini and Grok models. OSINT methods enabled the collection and analysis of open-source data from various channels, including social networks, public databases, and web resources. Gemini provided deep text data analysis, pattern recognition, and forecasting, while Grok, developed by xAI, was used to process complex queries and generate accurate conclusions based on large volumes of information. The combination of these technologies significantly accelerated the investigative process, enhanced the accuracy of the findings, and uncovered connections that might have remained undetected using traditional methods.

9. References and Bibliography

1. Ministry of Industry and Trade of the RF. Resolution No. 1402 of May 27, 2026, ‘On the regulation of imports of high-tech products’.

2. Federal Customs Service of the RF. Report on the structure of dual-use goods imports for the first quarter of 2026.

3. U.S. Department of Commerce. Bureau of Industry and Security. ‘Update on Export Controls and Secondary Sanctions Against Russian Technology Procurement Networks’, June 2026.

4. Center for New American Security (CNAS). ‘The Shadow Pipeline: How Western AI Hardware Reaches Russia through South Asian Hubs’, April 2026.

5. Financial Times. ‘Underground Supply Chains: The Chinese Intermediaries Feeding Russia’s Military Machine’, May 12, 2026.

6. KRONOS Institute for Social Dynamics and Security. ‘Chinese AI: The Strategic Defeat of the Russian Federation in the 21st Century Technological Clash’, June 2026.

7. International Monetary Fund (IMF). ‘Russian Federation: Statistical Appendix on Trade Asymmetry and Yuanization’, May 2026.

8. Reuters. ‘Sberbank targets Huawei’s Ascend chips for its GigaChat AI infrastructure amid chip crunch’, May 2024.

9. Yakov and Partners. ‘Artificial Intelligence in Russia: Economic Impact Assessment and Infrastructure Deficit by 2030’, February 2026.

10. CNews. ‘Baikal Electronics begins mass assembly of Baikal-U microcontrollers on RISC-V architecture’, March 2026.

11. Kommersant. ‘TSMC and the Russian Silicon: The Collapse of Domestic Microchip Production Contracts’, September 2024.

12. Vedomosti. ‘Varton Group acquires assets of bankrupt Baikal Electronics’, November 2025.

13. Habr. ‘The Russian Lithography: 130nm Prototypes and the Search for ASML Legacy Equipment’, January 2026.

14. McKinsey & Company / Yakov & Partners joint report. ‘AI Horizons: Transforming Russian Industries under Sanctions Constraint’, March 2026.

15. Yandex Press Service. ‘Alice AI 1.0 and the Integration of Generative Agents in Search Architecture’, February 2026.

16. SEO News. ‘The Death of Organic Traffic: How Yandex’s Transition to Generative Search Answers Reshaped SEO in 2026’, April 2026.

17. RBC Technology. ‘Russian B2B Cloud Platforms Migrate to Chinese Hardware Infrastructure’, May 2026.

18. Habr. ‘DeepSeek and Qwen: How Chinese Open-Source LLMs Became the Backbone of Russian Enterprise AI’, June 2026.

19. Sberbank Press Release. ‘GigaChat 3.0: Enhancing Russian Conversational AI and Kandinsky 5.0 Visual Synthesis’, April 2026.

20. Vedomosti. ‘Sberbank integrates AI interfaces into its ATM network’, May 2026.

21. Sberbank Tech Blog. ‘Introducing GigaChat Ultra and GigaAM-v3 Speech Synthesis’, March 2026.

22. Russia AI Benchmark Initiative. ‘Independent Evaluation of Reasoning Modes in Russian LLMs: GigaChat vs YandexGPT’, May 2026.

23. Stockholm International Peace Research Institute (SIPRI). ‘The Machine Tool Trap: Chinese Dominance in Russian Defense Production Lines’, June 2026.

24. Center for Strategic and International Studies (CSIS). ‘Chokehold: Huawei and ZTE’s Control Over Russia’s Telecommunication Backbone’, March 2026.

25. National Mining Association of Russia. ‘Rare Earth Metals: Tomtor Deposit Development and China’s Monopoly Processing Grid’, April 2026.

26. Council on Foreign Relations. ‘The Northern Sea Route: Russia’s Arctic Ambitions and Chinese Icebreaker Diplomacy’, January 2026.

27. Institute for the Study of War (ISW). ‘Refinery Warfare: The Economic Impact of Ukrainian Deep Strikes on Russian Energy Infrastructure’, May 2026.

28. Harvard Davis Center. ‘The Silent Annexation: Chinese Demographic and Agrarian Infiltration in the Russian Far East’, March 2026.

29. Center for European Policy Analysis (CEPA). ‘The Chinese Protectorate: Anticipating Moscow’s Socio-Political Succession Crisis’, February 2026.

30. Kyiv School of Economics (KSE). ‘Yuanization and Secondary Sanctions: The Breakdown of Russia-China Financial Pipelines’, June 2026.